Few will forget the last 18 months, as manufacturing and engineering businesses showed their resilience by adapting as quickly as possible to the new situation. On top of that, we’ve also had the challenge of coping with an exit from Europe that has been anything but simple.

Things have moved quickly – the UK has, at the time of writing, administered a first dose of the vaccine to over 45 million people, the final stages of the third national lockdown are being lifted and there was a last-minute deal on Brexit. Whilst this was perhaps not the deal that might have been envisaged by the slogan ‘take back control’ and early 2021 has seen either ‘teething problems’ or ‘fundamental flaws’ exposed, depending on where you sit, it was a deal, nonetheless.

Against this backdrop, MHA MacIntyre Hudson asked manufacturing and engineering companies in the UK if their views of the pandemic and Brexit had changed over the last six months and whether their initial thoughts when asked last year had been right.

When looking at how long it would take entities to return to their trading level pre-COVID, the most recent set of answers has seen the timescales lengthen a little with between six and 12 months and 12 and 24 months now representing 66% of the surveyed population against 62% last time.

Each of those answers has, individually, increased by 2% and the fall has been in the less than six month category which fell from 28% to 24%. This starts to underline the lengthening of the impact that business has felt and is, I suspect, coloured by the setbacks of successive lockdowns across the country.

The longer impact felt from COVID is also, perhaps, echoed in responses concerning investment plans for the next 12 months.

Whilst the majority (75%) are planning to invest less (significantly or slightly) or the same as planned, this number has fallen from 81% six months ago, perhaps indicating that business will have to invest further to overcome the impact that COVID has had upon business.

The individual largest response remains unchanged at 31% being that investment plans will proceed as planned but 24%, as opposed to 19%, are looking to invest slightly or significantly more.

However, with recent measures announced by the Chancellor that are aimed at encouraging investment, we will look with interest as to whether these will achieve their aim.

We also asked whether respondents had changed their product mix as a result of the pandemic. The answers remained virtually unchanged with 51%, as opposed to 50%, saying ‘no’.

This, of course, can be interpreted from both directions and, of the 49% who have changed, 32% have done so by a little, 10% by quite a lot, and 7% significantly.

Turning to the specific impact of COVID inside the workplace, we asked whether social distancing had affected production capacity. Whilst there was no change in those (51%) who said ‘a little’ there has been a significant shift, a fall from 27% to 24%, in those who have not been affected and an increase from 9% to 18% of businesses being impacted ‘quite a lot’. Again, this perhaps underlines the longer impact of COVID upon businesses than originally anticipated.

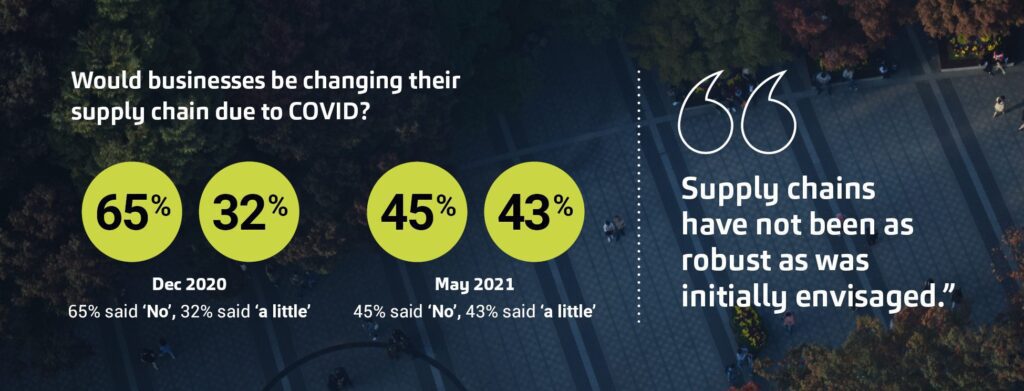

Many of our conversations with manufacturing and engineering entities initially concentrated on the supply chain, and many businesses talked about shortening that in order to safeguard supplies. Our question was whether businesses would be changing their supply chain.

Our respondents’ views have seen a significant shift over the last six months. In our last report, 65% said ‘no’ and 32% said ‘a little’. This time, only 45% said ‘no’ and 43% said ‘a little’ perhaps indicating that the supply chains have not been as robust as was initially envisaged or, perhaps the impact of the Brexit deal has been seen more starkly.

The role of Government has been, and continues to be, unprecedented in peace time in terms of providing various types of state aid, so we asked how well manufacturing and engineering entities felt that they had been supported by Government during the pandemic.

Views in the centre ground have remained virtually unchanged over the last six months, where 45% felt that the Government had done enough.

The furlough scheme, in particular, was described by a respondent

as invaluable and around 28% felt that Government could do more with some form of rates relief appearing in various

of the comments in this regard.

The change in responses to this question has appeared at perhaps the extremes of the answers, with only 13%, as opposed to 21%, feeling that the Government’s response has been ‘fantastic’ and 10%, as opposed to 5% answering, when asked if they felt supported by the Government, ‘not at all’.

In terms of the impact of a Brexit deal, we asked respondents if they have had to change business practices as a result of the Brexit agreement. Perhaps not surprisingly the response was ‘yes’ from 61% of respondents, particularly in terms of additional paperwork.

Various respondents commented that the lateness of the deal had left them little time to prepare and that none of HMRC, couriers or freight carriers appeared to know what was required, certainly initially.

Many also commented on the cost of this, whether that be in time completing paperwork declarations for which they could not charge, delays in materials being supplied and exports clearing the ports, and the cost implicit in this, or some goods being diverted around the UK’s borders. This is a point that we feel needs to be monitored and addressed by Government.

As a follow up to this we asked whether businesses had seen friction or obstacles as a result of the Brexit agreement when trading with the EU or with Northern Ireland, and 56% said ‘no’.

So, what can we conclude from these responses?

Clearly it is evident, and to some degree not unexpected, that the pandemic, combined with Brexit, has changed manufacturing and engineering businesses’ continued transition to a ‘new normal’.

The ability of manufacturers and engineers to pivot has been much in evidence and the continued review and strengthening of supply chains is important.

However, the impact on businesses of COVID has been more significant than was first thought.

The role of Government has been unprecedented and with the measures announced in the last Budget we continue to see this significant support into businesses from the pandemic.

That said, there has been well-publicised disruption and cost from the Brexit agreement and, more recently, raw material and labour shortages that have affected many manufacturers and engineers so as 2021 unfolds the challenges continue for this vital section of our economy.

For more information, visit MHA and Bakertilly International.